Insights

Find the latest news and insights from TrueShares below.

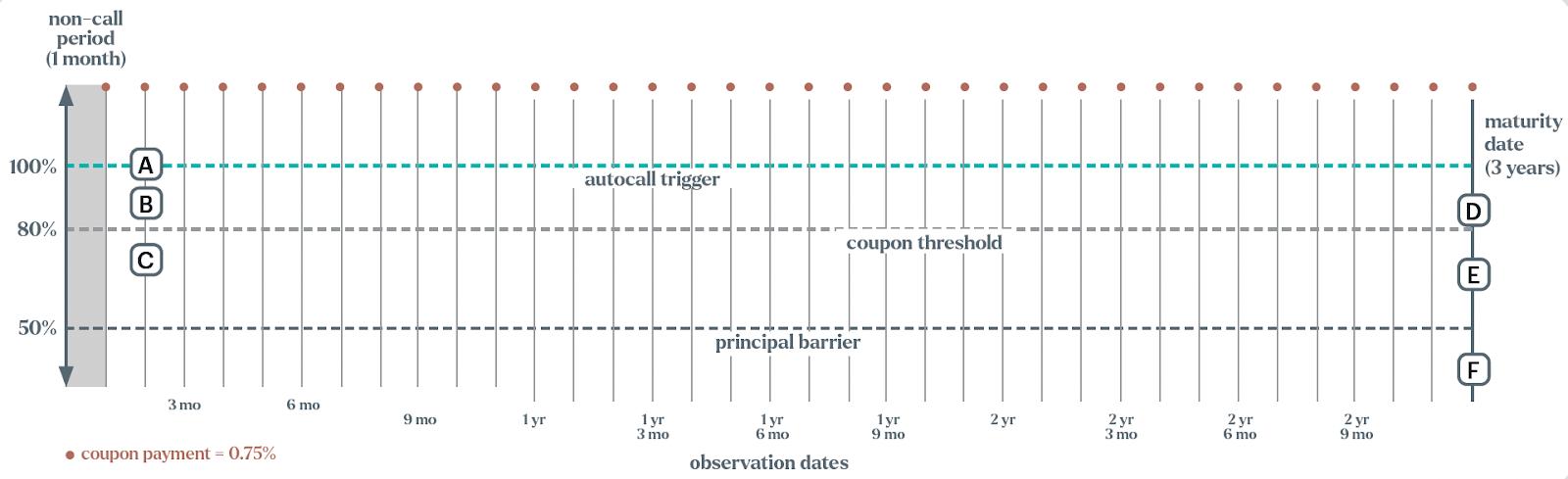

Potential Outcomes for an Autocallable Note

What used to be reserved only for institutional and high net-worth individuals is now more readily available than ever. Several new autocallable ETFs, like TrueShares S&P Autocallable Income ETFs, are now on the market and intriguing investors with their potential.

These autocallable ETFs are based on the performance of a reference index over a set term period, with clearly defined parameters designed to provide stable, high monthly income if those parameters are met. It’s all about thresholds, barriers, triggers, and coupons, all of which are set from the inclusion of an autocallable in a portfolio. To better understand what might happen in different market scenarios, we’ve broken the concept down into several potential scenarios for a single autocallable.

To refresh yourself on the terms, see What are Autocallables.

Let’s consider a 3-year autocallable, with a non-callable period of one month, coupon of 9%, annualized (fixed income component), a coupon threshold of 80% of the value of the reference index, and a principal barrier of 50% of the value of the reference index.

At the end of 2 months (the next observation date after the non-call period), there are 3 potential scenarios that could take place with the autocallable (see above):

- If the reference index is 100% of its initial value or more, the autocall trigger has been breached for that autocallable and the autocallable is called. The investor receives their full principal back, plus the coupon payment for that observation period.

- If the reference index is between 80-100% of its initial value, the investor receives their coupon payment for that observation period and the autocallable continues.

- If the reference index is less than 80% of its initial value, the coupon barrier has been breached and the fund does not receive the coupon payment for that observation period, but the autocallable continues.

At the end of 3 years (at maturity), assuming the autocall trigger has not been breached at any monthly observation date, there are 3 potential outcomes of that autocallable (see above):

- If the reference index is between 80-100% of its initial value, the investor is repaid the entirety of their principal and still receives the final coupon payment for the last observation period. The investor still receives their coupon payment because it has not fallen enough to breach the coupon threshold of 80%.

- If the reference index is less than 80% of its initial value, the investor is repaid the entirety of their principal, but does not receive a coupon payment for that observation period. The investor receives their principal because the value of the reference index is above the principal barrier of 50%, but the investor does not receive their coupon payment because the value of the reference index has fallen enough to breach the coupon threshold of 80%.

- If the reference index is 50% or less of its initial value, the investor receives a reduced principal repayment and does not receive a coupon payment for that observation period. For example, if the reference index is 40% of its initial value, then 40% of the initial principal will be repaid.

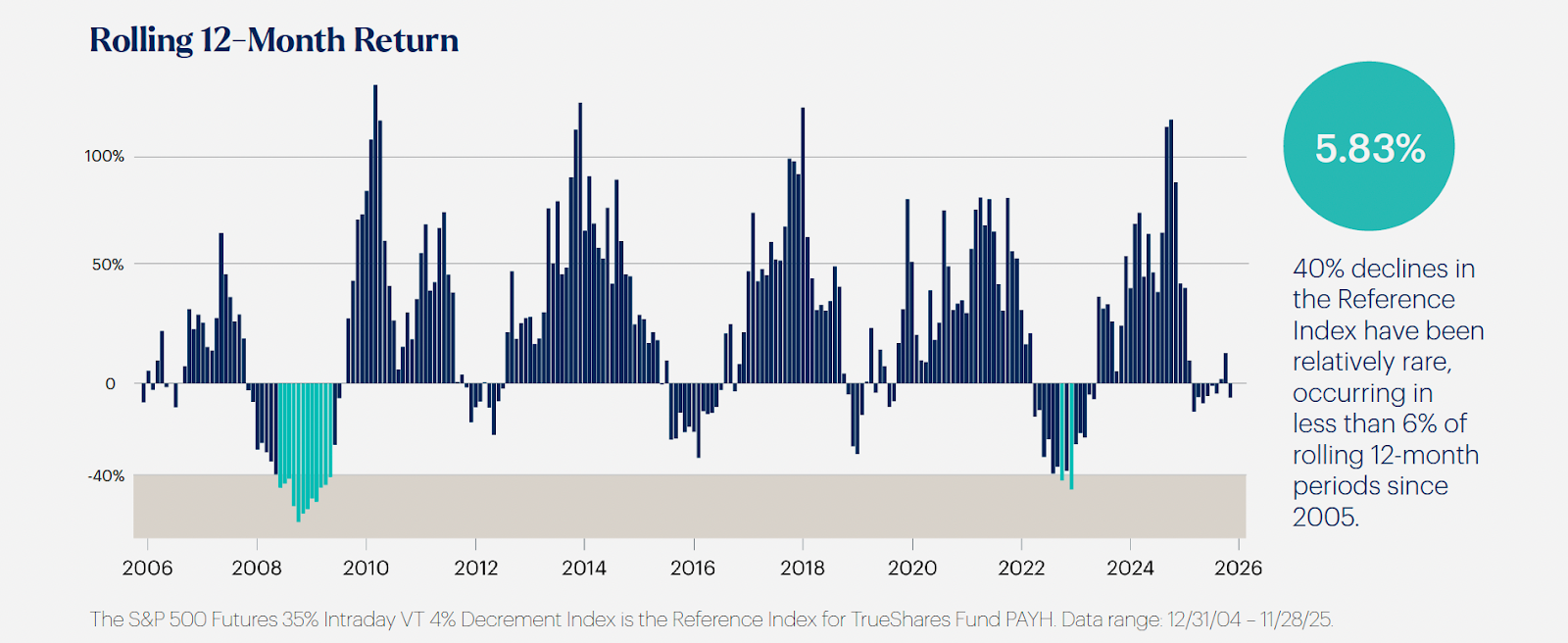

All autocallables expose the principal investment to market losses if the reference index falls below the principal barrier at maturity. Now consider a principal barrier of 60% of the reference index, meaning the value of the reference index would have to drop 40% below its initial value for the investor to start losing any of their principal investment.

How often has the market, historically, dropped 40%? Only 5.83% of the time in the last two decades.

In the vast majority of markets (historically), principal investments in an autocallable product are preserved. An ETF of autocallables smooths the ride even more than a single autocallable by combining multiple autocallables into a single portfolio. Even if one autocallable falls below the coupon threshold or principal barrier, the other autocallables are there to level out the portfolio, potentially providing even more downside protection. Autocallable ETFs focus on providing stable income and returning the principal, even if that means the market is down.

TrueShares offers two new autocallable ETFs, the S&P Autocallable High Income ETF (PAYH) and the S&P Autocallable Defensive Income ETF (PAYM). PAYH and PAYM bring the popular autocallable income strategy to investors seeking high, stable monthly income. The ETF wrapper seeks to offer predictable income, contingent protection, and built-in hedging, all in a tax efficient single-ticker solution.

To learn more about the funds, visit: https://www.true-shares.com/autocallable-income-etfs

.jpg)

.jpg)

Thought Leadership,

Straight to Your Inbox

Disclosures

©2026, TrueShares, ©2026 TrueMark Investments, LLC. (“TrueMark”).

Before investing, carefully consider the TrueShares ETFs investment objectives, risks, charges and expenses. Specific information about TrueShares is contained in the prospectus and a summary prospectus, copies of which may be obtained by visiting www.www.true-shares.com. Read the prospectus carefully before you invest.

An investment in TrueShares is subject to numerous risks, including possible loss of principal. The ETFs are subject to the following principal risks: Authorized Participants, Market Makers, and Liquidity Providers Concentration Risk associated with ETFs; Equity Market Risk; Management Risk; Market Capitalization Risk (Large Cap; Mid Cap, Small Cap Stock); Market Risk; New Fund Risk: The Fund is a recently organized, non-diversified management investment company with no operating history. As a result, prospective investors have no track record or history on which to base their investment decision. Additionally, the Adviser has not previously managed a registered fund, which may increase the risks of investing in the Fund.

Depositary Receipts Risk. American Depositary Receipts (“ADRs”) have risks similar to those of foreign securities (political and economic conditions, changes in the exchange rates, etc.) and entitle the holder to all dividends and capital gains that are paid out on the underlying foreign shares.

Individual investors should contact their financial advisor or broker dealer representative for more information on TrueShares ETFs.

Investment Products and Services are: NOT FDIC INSURED / MAY LOSE VALUE / NO BANK GUARANTEE.

All registered investment companies, including TrueShares, are obliged to distribute portfolio gains to shareholders at year-end regardless of performance. Trading in TrueShares ETFs will also generate tax consequences and transaction expenses. The information provided is not intended to be tax advice. Tax consequences of dividend distributions may vary by individual taxpayer.

TrueShares ETFs are bought and sold through exchange trading at market price, not Net Asset Value (NAV), and are not individually redeemed from the fund. Shares may trade at a premium or discount to their NAV in the secondary market. Brokerage commissions will reduce returns.

ETF shares may be bought or sold throughout the day at their market price, not their NAV, on the exchange on which they are listed. Shares of ETFs are tradable on secondary markets and may trade either at a premium or a discount to their NAV on the secondary market. ETFs trade like stocks, fluctuate in market value and may trade at prices above or below the ETF’s NAV. Brokerage commissions and ETF expenses will reduce returns.

Fund Intelligence Mutual Fund Industry and ETF Award shortlists and winners are comprised of individuals and firms who have submitted entries or been nominated via the online submission process, as well as through recommendations from leading market participants. Fund Intelligence Mutual Fund Industry and ETF Award judges will use the submitted application material, as well as any uploaded supplemental information, to determine which firm, individual or product they believe to be the most suitable and deserving winners for each category. Fund Intelligence Mutual Fund Industry and ETF Award judges have the discretionary power to move nominations into alternative categories that they think may be more suitable. Fund Intelligence Mutual Fund Industry and ETF Awards were decided by an independent panel of 20 judges with expertise across the asset management space.

TrueShares ETFs (the “Funds”) are registered with the United States Securities and Exchange Commission under the Investment Company Act of 1940. The fund is distributed by Paralel Distributors LLC, Member FINRA. Paralel is not affiliated with TrueMark Investments, LLC. TrueMark Investments, LLC, is the investment advisor to the Funds and receives a fee from the Funds for its services.

TrueMark Investments, LLC is the investment advisor to the Funds and receives a fee from the Funds for its services.

TrueShares ETFs are offered only to United States residents, and information on this site is intended only for such persons. Nothing on this website should be considered a solicitation to buy nor an offer to sell shares of any fund in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction.