Insights

Find the latest news and insights from TrueShares below.

Increased Grid Access for Renewables Boosts Adoption

It’s High Time We Let Energy Infrastructure Get Some

President Eisenhower signed the Federal-Aid Highway Act in 1956, which led to the investment and construction of 41,000 miles of highways over a 10-year period. More recently there has been a flurry of legislation passed targeting various industries, such as the Inflation Reduction Act for renewable energy and the CHIPS Act for semiconductors. While Congress is in the mood, we think they should let energy infrastructure get some too. At the top of the energy infrastructure wish list is a bigger and better electric grid, as we believe its current limitations will inevitably make it the biggest barrier to energy transition. Without upgrades and expansions to the grid, we will end up with less renewable energy, more emissions, and a higher probability for human-made and natural catastrophes.

The reason why there is a car in every driveway and a chicken in every pot is because of scale. Scale is the great provider of things, allowing a developer to incorporate the best technology and, most important, drives unit costs lower. Scale is the major reason why the cost of renewable energy is now below fossil fuels. However, there is a limit to how much you can achieve without running into new bottlenecks. Scale requires space, preferably inexpensive. This tends to be in rural areas where space is at a discount, therefore, the problem we need to solve today is the delivery of cheap electricity to market. Think about it, where would Amazon be if it couldn’t efficiently deliver products to market? If we expect to achieve our energy transition goals the renewable energy sector must dedicate the same amount of attention to delivery as Amazon does.

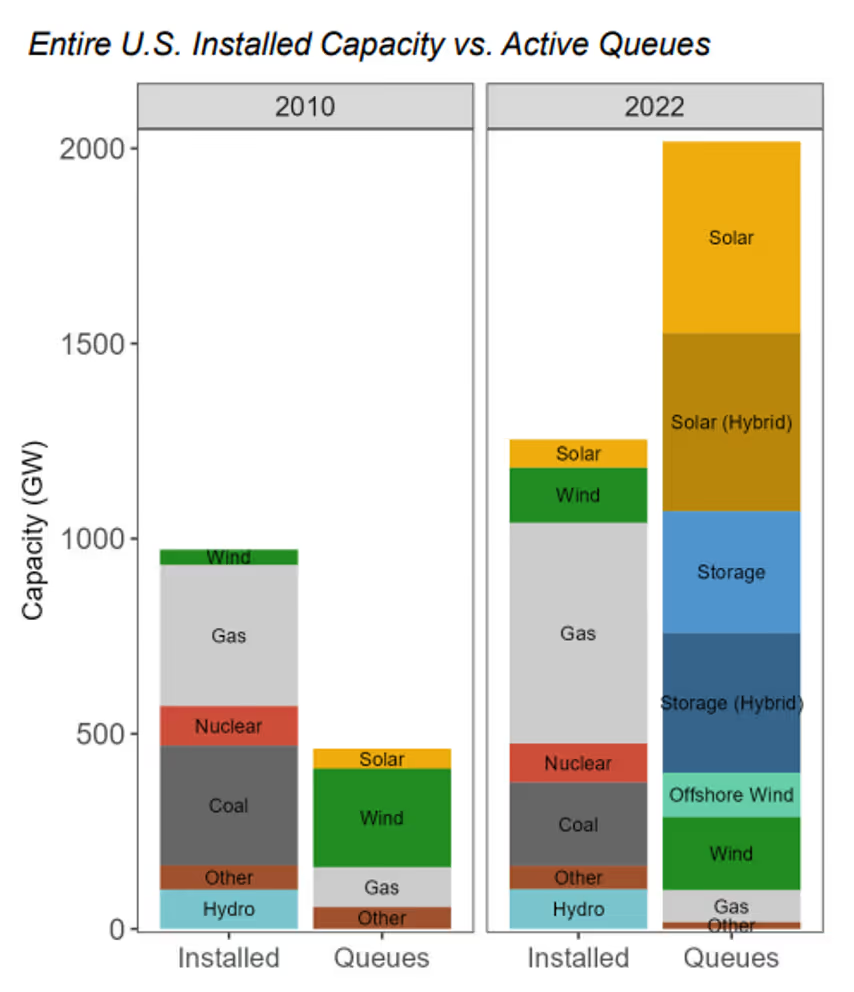

The current wait time in the interconnection queue for new power generation or storage is over five years, up from less than two years in 2008. In fact, at the end of 2022 there were more than 2,000 gigawatts waiting to be connected across the United States, an amount that if built would double the nation’s current generation capacity (double!). Therefore, it was likely with great relief to both electric generation developers and grid operators that the U.S. Federal Energy Regulatory Commission (FERC) unanimously approved a final rule in July reforming interconnection procedures and agreements. This reform is a great victory for renewable energy since the vast majority (>90%) of the queue is zero carbon-focused infrastructure.

Source: Lawrence Berkeley National Laboratory

Even so, more needs to be done. The grid is inadequate and outdated. More than 70% of the US electricity grid is more than 25 years old, with most infrastructure having been built in the 1950s and 1960s. This all matters because an upgraded and larger grid is necessary to provide three critical ingredients of energy transition: reliability, affordability, and sustainability.

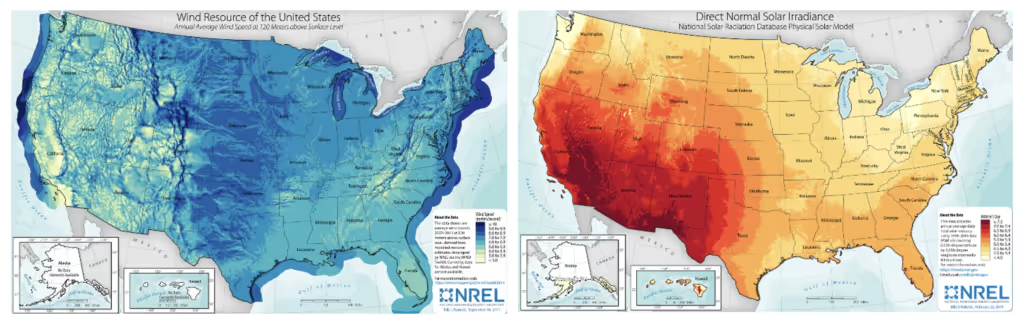

Reliability. While renewable energy costs on a per MWh basis have declined below fossil fuels, that’s only when renewable energy is generating electricity. Generally speaking windmills are spinning roughly 40% of the time and solar fields are delivering electricity roughly 25% of the time. This mismatch can be partially dealt with a more integrated and expansive grid and the incorporation of energy storage (e.g., batteries). Power load management is only possible if load managers can build systems that are capable of delivering electricity from areas with surplus generation to areas with excess demand. Reliability is critical to delivering a seamless customer experience, which will make for a smoother and quicker energy transition.

Source: National Renewable Energy Laboratory

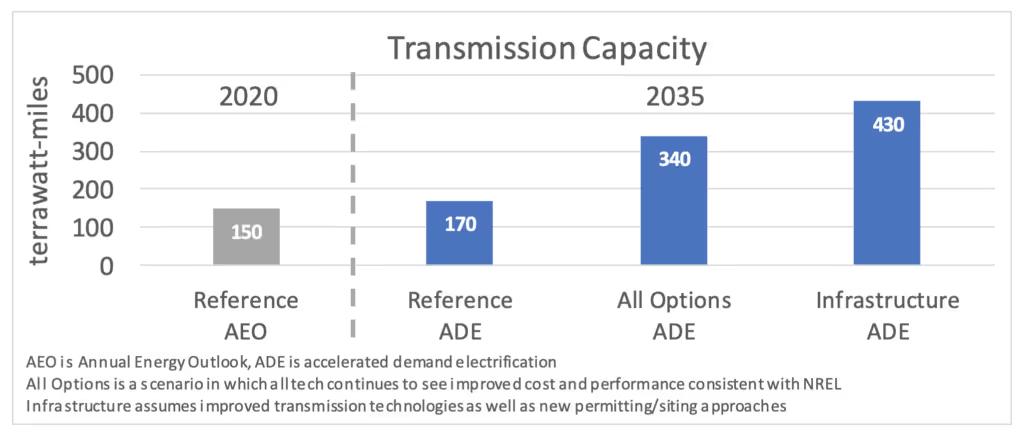

Affordability. Economies of scale on renewable energy generation will only go as far as the next bottleneck. The FERC action detailed above helps shorten the line for generation projects, but it won’t do much to increase or enhance transmission capacity. The National Renewable Energy Laboratory (NREL) suggests a doubling or tripling of transmission capacity is needed to achieve 100% clean energy, a need that currently lacks plans or incentives to accelerate. Without adequate transportation to market, economies of scale won’t be fully realized, and some renewable energy generation will not be built.

Source: National Renewable Energy Laboratory

Sustainability. Reliability and Affordability are the two major foundations of consumer buy-in. Buy-in is basically the idea that consumers will not support energy transition if their lives are degraded by a lack of energy. Delivering reliable and affordable renewable energy will secure this buy-in, which allows developers and regulators to approve more renewable energy projects.

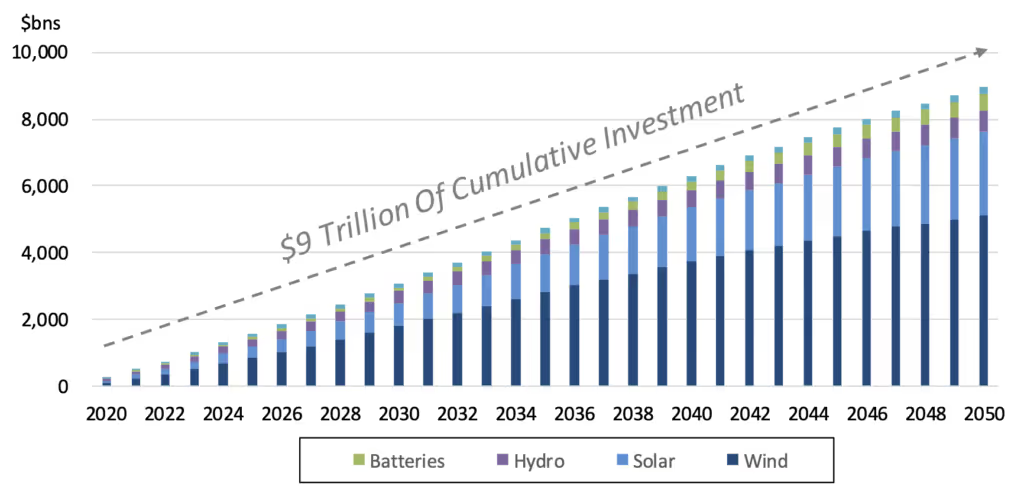

In summary, the government is incentivizing trillions of dollars of investment in renewable energy over the next several decades. It would be a shame to miss our energy transition goals due to a lack of investment in energy infrastructure. Better yet is the ample room for compromise, since the vast middle agrees that all forms of energy and innovation are needed to solve our climate challenges. It’s high time for energy infrastructure to get some.

Source: Bloomberg New Energy Finance

Mike Cerasoli is the Co-Head of Eagle Global’s Energy Infrastructure team, which focuses on and develops active and passive asset management strategies in traditional and renewable energy infrastructure. Eagle Global Advisors, LLC is an independent investment advisor, managing individual investment portfolios containing domestic equity, international equity, energy infrastructure and master limited partnerships, and domestic fixed income securities. For more information, please visit www.eagleglobal.com.

.jpg)

.jpg)

Thought Leadership,

Straight to Your Inbox

Disclosures

©2026, TrueShares, ©2026 TrueMark Investments, LLC. (“TrueMark”).

Before investing, carefully consider the TrueShares ETFs investment objectives, risks, charges and expenses. Specific information about TrueShares is contained in the prospectus and a summary prospectus, copies of which may be obtained by visiting www.www.true-shares.com. Read the prospectus carefully before you invest.

An investment in TrueShares is subject to numerous risks, including possible loss of principal. The ETFs are subject to the following principal risks: Authorized Participants, Market Makers, and Liquidity Providers Concentration Risk associated with ETFs; Equity Market Risk; Management Risk; Market Capitalization Risk (Large Cap; Mid Cap, Small Cap Stock); Market Risk; New Fund Risk: The Fund is a recently organized, non-diversified management investment company with no operating history. As a result, prospective investors have no track record or history on which to base their investment decision. Additionally, the Adviser has not previously managed a registered fund, which may increase the risks of investing in the Fund.

Depositary Receipts Risk. American Depositary Receipts (“ADRs”) have risks similar to those of foreign securities (political and economic conditions, changes in the exchange rates, etc.) and entitle the holder to all dividends and capital gains that are paid out on the underlying foreign shares.

Individual investors should contact their financial advisor or broker dealer representative for more information on TrueShares ETFs.

Investment Products and Services are: NOT FDIC INSURED / MAY LOSE VALUE / NO BANK GUARANTEE.

All registered investment companies, including TrueShares, are obliged to distribute portfolio gains to shareholders at year-end regardless of performance. Trading in TrueShares ETFs will also generate tax consequences and transaction expenses. The information provided is not intended to be tax advice. Tax consequences of dividend distributions may vary by individual taxpayer.

TrueShares ETFs are bought and sold through exchange trading at market price, not Net Asset Value (NAV), and are not individually redeemed from the fund. Shares may trade at a premium or discount to their NAV in the secondary market. Brokerage commissions will reduce returns.

ETF shares may be bought or sold throughout the day at their market price, not their NAV, on the exchange on which they are listed. Shares of ETFs are tradable on secondary markets and may trade either at a premium or a discount to their NAV on the secondary market. ETFs trade like stocks, fluctuate in market value and may trade at prices above or below the ETF’s NAV. Brokerage commissions and ETF expenses will reduce returns.

Fund Intelligence Mutual Fund Industry and ETF Award shortlists and winners are comprised of individuals and firms who have submitted entries or been nominated via the online submission process, as well as through recommendations from leading market participants. Fund Intelligence Mutual Fund Industry and ETF Award judges will use the submitted application material, as well as any uploaded supplemental information, to determine which firm, individual or product they believe to be the most suitable and deserving winners for each category. Fund Intelligence Mutual Fund Industry and ETF Award judges have the discretionary power to move nominations into alternative categories that they think may be more suitable. Fund Intelligence Mutual Fund Industry and ETF Awards were decided by an independent panel of 20 judges with expertise across the asset management space.

TrueShares ETFs (the “Funds”) are registered with the United States Securities and Exchange Commission under the Investment Company Act of 1940. The fund is distributed by Paralel Distributors LLC, Member FINRA. Paralel is not affiliated with TrueMark Investments, LLC. TrueMark Investments, LLC, is the investment advisor to the Funds and receives a fee from the Funds for its services.

TrueMark Investments, LLC is the investment advisor to the Funds and receives a fee from the Funds for its services.

TrueShares ETFs are offered only to United States residents, and information on this site is intended only for such persons. Nothing on this website should be considered a solicitation to buy nor an offer to sell shares of any fund in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction.