Insights

Find the latest news and insights from TrueShares below.

Where are all the Dividends?

The year is 1999. Markets are awash with talk of the dot com boom. Tech companies are raging forward at breakneck speed. Growth is their north star. Their valuations are inflated. The bubble is about to burst.

And burst it did.

Some might be tempted to say that we appear to be repeating ourselves with the current AI boom, but many differences separate us from our past. Yes, the market is being driven by big tech companies. And yes, many of them seem overvalued. They are, however, more profitable than their 1990s forebears. Yet one main commonality that investors are clocking is the serious lack of dividends being offered by tech companies today and in the late 90s.

Companies typically offer dividends to shareholders as compensation for taking on the risk of investing. They usually provide quarterly income that can be cashed out or reinvested to compound on itself over time. But as growth took over in the 1990s, dividend yield dropped to an all-time low of 1.15%.1 This matters because dividends have historically made up a significant portion of total return for the S&P 500 — 34% on average from 1940 to 2024.2 Without high dividend yield, returns suffer. Their near total absence (a mere 1.8% annualized return)2 post-bubble burst is believed to have contributed to the “subpar” returns of the lost decade.1

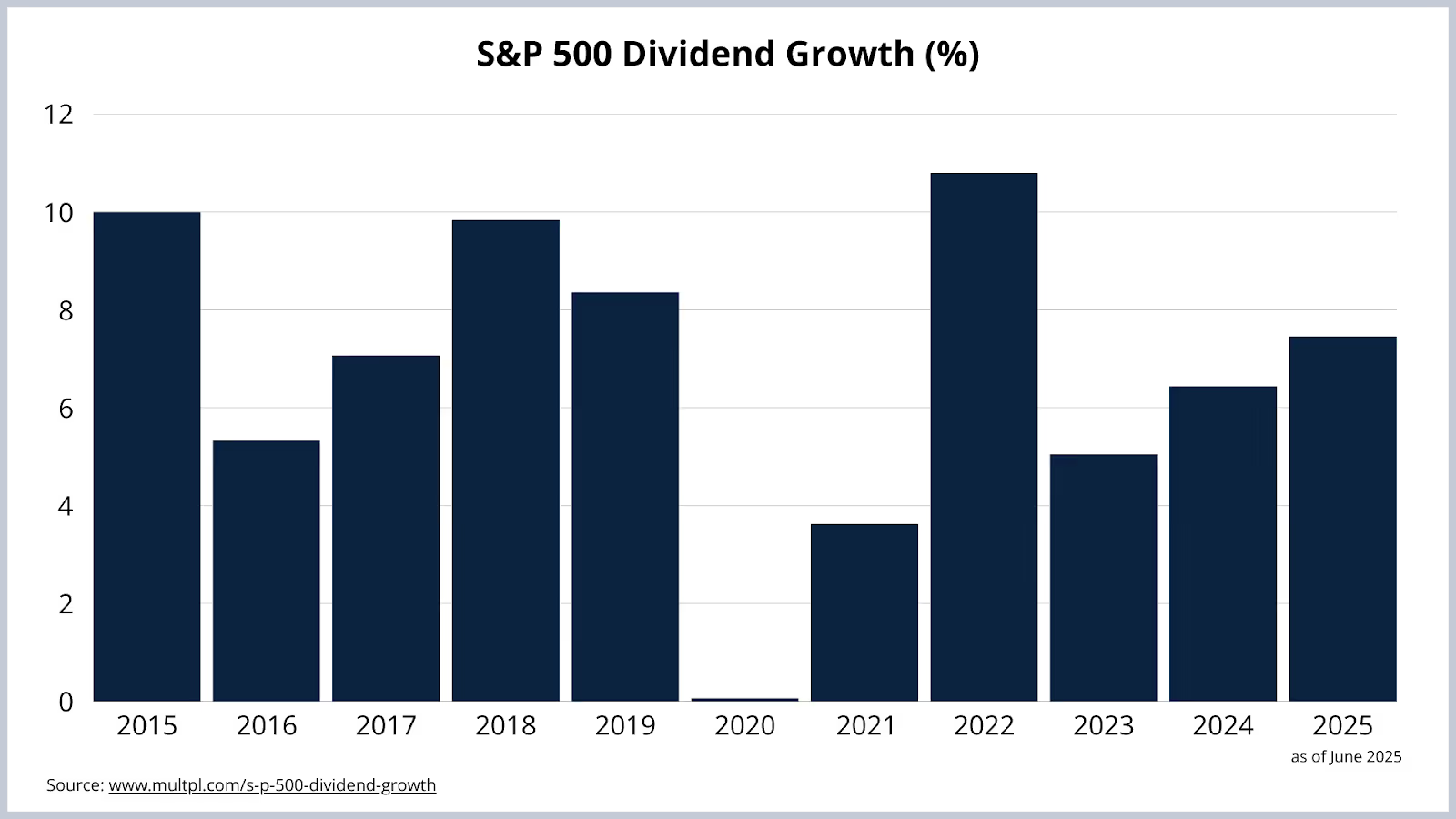

And yet here we are again, nearing the all-time dividend lows of the early aughts. As of June 2025, S&P 500 dividend yield was 1.25%.3 But that doesn’t mean dividends are gone. It just means the big tech companies driving S&P 500 returns are focused on hyper-growth instead of certain fundamentals like dividends. They are issuing stock buybacks instead and using their cashflow to invest heavily in AI.4 It’s now more important than ever to look for investments with high-quality and/or high-yield dividends.

Because dividends still matter.

Dividends contributed 17% of total S&P 500 returns in the 2010s and 12% in the 2020s (as of Dec. 31, 2024.)2 Dividends matter the most for the companies issuing them. Compared to companies that cut or eliminated dividends from 1973 to 2024, the companies that initiated or increased their dividends experienced higher returns with less volatility.2 They also tend not to cut dividends as quickly as buybacks during market dips or times of high volatility. If anything, companies tend to grow their dividends over time.

When added to a portfolio, dividends help buffer against volatility because they are a strong signal of a company’s long-term health.4 Adding a dividend ETF to one’s portfolio helps diversification* so that if tech doesn’t continue to perform as expected or one’s financial goals shift, there’s a potential income component waiting in the wings.

Looking for distinct dividend ETF strategies for a diversified portfolio?

TrueShares Featured Funds:

- Opal Dividend Income ETF (DIVZ): Highly concentrated in high-quality, dividend-providing, domestic companies. Seeks above-average dividend yield and below-average volatility with monthly distributions.

- Opal International Dividend Income ETF (IDVZ): Highly concentrated in high-quality, dividend-providing, international companies. Seeks above-average dividend yield and below-average volatility with monthly distributions.

- TrueShares Active Yield ETF (ERNZ): An actively-managed fund aiming to provide consistent income by focusing on high-yield without sacrificing valuation.

- https://www.latimes.com/archives/la-xpm-2001-sep-30-fi-51481-story.html

- https://www.hartfordfunds.com/insights/market-perspectives/equity/the-power-of-dividends.html

- https://ycharts.com/indicators/sp_500_dividend_yield

- https://finance.yahoo.com/news/where-have-all-the-dividends-gone-123021534.html

Disclosures:

*Diversification does not ensure a profit nor protect against loss in a declining market.

Thought Leadership,

Straight to Your Inbox

Disclosures

©2025, TrueShares, ©2025 TrueMark Investments, LLC. (“TrueMark”).

Before investing, carefully consider the TrueShares ETFs investment objectives, risks, charges and expenses. Specific information about TrueShares is contained in the prospectus and a summary prospectus, copies of which may be obtained by visiting www.www.true-shares.com. Read the prospectus carefully before you invest.

An investment in TrueShares is subject to numerous risks, including possible loss of principal. The ETFs are subject to the following principal risks: Authorized Participants, Market Makers, and Liquidity Providers Concentration Risk associated with ETFs; Equity Market Risk; Management Risk; Market Capitalization Risk (Large Cap; Mid Cap, Small Cap Stock); Market Risk; New Fund Risk: The Fund is a recently organized, non-diversified management investment company with no operating history. As a result, prospective investors have no track record or history on which to base their investment decision. Additionally, the Adviser has not previously managed a registered fund, which may increase the risks of investing in the Fund.

Depositary Receipts Risk. American Depositary Receipts (“ADRs”) have risks similar to those of foreign securities (political and economic conditions, changes in the exchange rates, etc.) and entitle the holder to all dividends and capital gains that are paid out on the underlying foreign shares.

Individual investors should contact their financial advisor or broker dealer representative for more information on TrueShares ETFs.

Investment Products and Services are: NOT FDIC INSURED / MAY LOSE VALUE / NO BANK GUARANTEE.

All registered investment companies, including TrueShares, are obliged to distribute portfolio gains to shareholders at year-end regardless of performance. Trading in TrueShares ETFs will also generate tax consequences and transaction expenses. The information provided is not intended to be tax advice. Tax consequences of dividend distributions may vary by individual taxpayer.

TrueShares ETFs are bought and sold through exchange trading at market price, not Net Asset Value (NAV), and are not individually redeemed from the fund. Shares may trade at a premium or discount to their NAV in the secondary market. Brokerage commissions will reduce returns.

ETF shares may be bought or sold throughout the day at their market price, not their NAV, on the exchange on which they are listed. Shares of ETFs are tradable on secondary markets and may trade either at a premium or a discount to their NAV on the secondary market. ETFs trade like stocks, fluctuate in market value and may trade at prices above or below the ETF’s NAV. Brokerage commissions and ETF expenses will reduce returns.

Fund Intelligence Mutual Fund Industry and ETF Award shortlists and winners are comprised of individuals and firms who have submitted entries or been nominated via the online submission process, as well as through recommendations from leading market participants. Fund Intelligence Mutual Fund Industry and ETF Award judges will use the submitted application material, as well as any uploaded supplemental information, to determine which firm, individual or product they believe to be the most suitable and deserving winners for each category. Fund Intelligence Mutual Fund Industry and ETF Award judges have the discretionary power to move nominations into alternative categories that they think may be more suitable. Fund Intelligence Mutual Fund Industry and ETF Awards were decided by an independent panel of 20 judges with expertise across the asset management space.

TrueShares ETFs (the “Funds”) are registered with the United States Securities and Exchange Commission under the Investment Company Act of 1940. The fund is distributed by Paralel Distributors LLC, Member FINRA. Paralel is not affiliated with TrueMark Investments, LLC. TrueMark Investments, LLC, is the investment advisor to the Funds and receives a fee from the Funds for its services.

TrueMark Investments, LLC is the investment advisor to the Funds and receives a fee from the Funds for its services.

TrueShares ETFs are offered only to United States residents, and information on this site is intended only for such persons. Nothing on this website should be considered a solicitation to buy nor an offer to sell shares of any fund in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction.