From Eagle Global Advisors

A Furious 4Q Rally Offsets 3Q Despair; Cautiously Optimistic For 2024

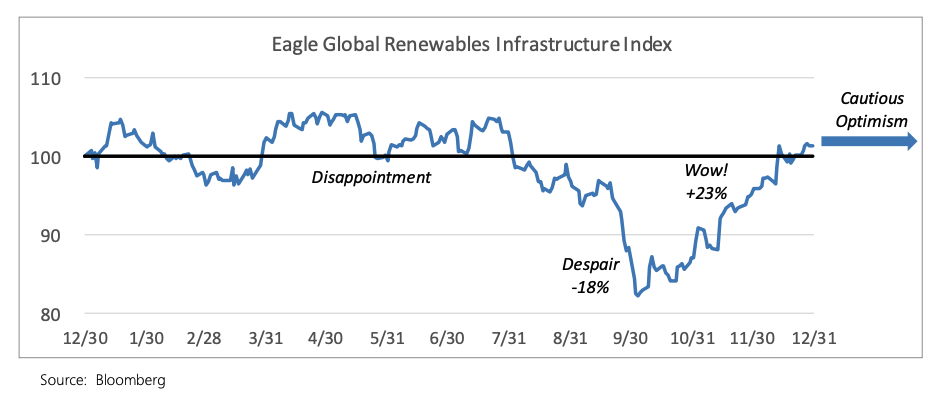

The Eagle Global Renewables Infrastructure Index (Bloomberg ticker: RENEW; Factset ticker: RENEWINDEX) generated positive absolute total return performance in 2023 (+1%). This resulted from a furious fourth quarter rally (+23%) that started with the U.S. Federal Reserve’s shift towards interest rate stabilization and the potential for rate reductions in 2024. This welcome relief countered the despair that encompassed the third quarter (-18%) as high interest rates, supply/equipment delivery delays, and cost overruns weighed heavily on renewables infrastructure. We’re cautiously optimistic on the sector heading into 2024 as we expect “jet stream” strong headwinds to finally dissipate after several years, which should allow companies to execute on the enormous growth needed to deliver energy transition. Our caution stems from the admitted perilousness of the broader market, which continues to remain at risk of recession, a return of inflation, and geopolitical turmoil.

Long-Term Déjà Vu, Short-Term Much Improved: Cautious Optimism For 2024

Our long-term view hasn’t changed, so expect déjà vu on how we view renewables infrastructure. That is, a highly supportive Main Street backed by Wall Street and government incentives is driving our society towards energy transition. It’s happening, and we believe renewables infrastructure offers the best risk-adjusted total return proposition within the renewables sector. Again, déjà vu.

What has changed dramatically since the fourth quarter of 2022 and even just during the last quarter of 2023 is the short-term outlook, which is starting to look like a classic example of “it’s always darkest before the dawn”. Three months ago, we recognized this despair and suggested “if you ignore the noise you’ll find the root causes of these issues are near-term in nature and on their way to resolution.” We weren’t expecting stock performance to reverse as sharply as it did. With this in mind, we highlight interest rates, the one clear difference between then and now which could end up being the difference

maker.

The Difference Maker: Interest Rates

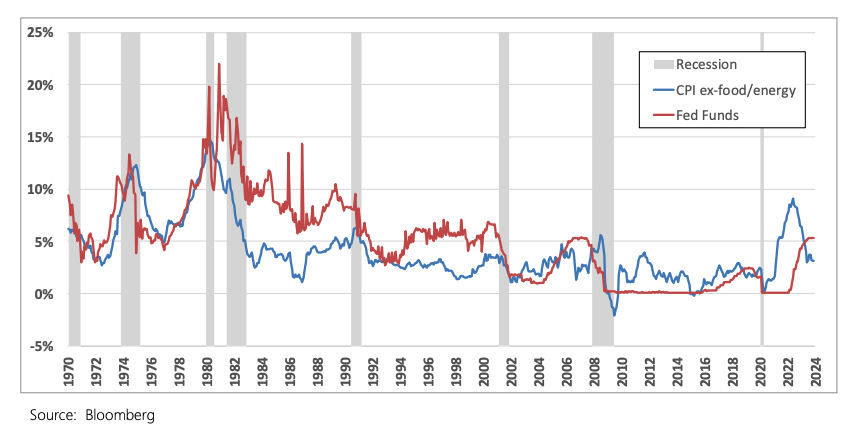

Over the course of several public comments, the U.S. Federal Reserve indicated first that they would suspend incremental rate hikes as inflation subsided, and then in early-December penciled in three rate cuts for 2024 to help support a slowing economy. Not surprisingly, growth stocks, like renewables infrastructure, rallied hard on these updates given the impact rising interest rates had on the sector’s ability to execute growth. This was especially true for those companies like Orsted, which signed contracts pre-pandemic and then failed to lock in financing and construction costs. For others it was more a question of scale, since capital is limited and high interest rates forced them to scale back the size and scope of their growth expectations.

We believe stable and perhaps declining interest rates – and the implication that inflation is under control – should reverse what had been a strong headwind into a modest tailwind. Companies rely on stability and a predictable investment environment to determine whether a project moves forward. Since a large majority of project financing comes from debt, interest rate stability is critical to helping companies get comfortable with return expectations and quantify risk.

The Supply Chain Question Mark

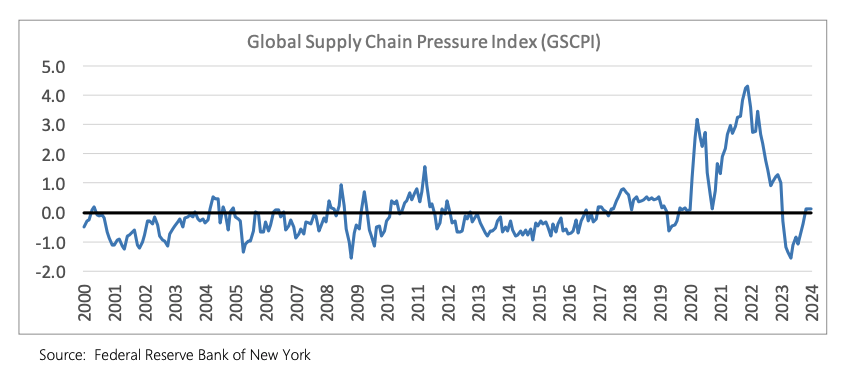

The supply chain has been a disappointment so far. The Federal Reserve Bank of New York’s Global Supply Chain Pressure Index surged during the pandemic, recovered briefly, and then surged again in 2021-22. Successful energy transition depends on the global manufacturing and transportation network to deliver products and equipment on time and on budget. Despite the data suggesting a resolution to supply chain issues, headlines within renewable energy suggested otherwise. As an example, Orsted in the third quarter revealed challenges securing critical equipment and supplies that resulted in a dramatic increase in project costs. Not surprisingly, Orsted’s stock took a major hit as a result of this. So while we’re hopeful the supply chain will improve in 2024 as the data from the NY FED suggests it already has, we’re still waiting for confirmation from our companies. Our fear is compounded by an increasingly strained geopolitical environment, where risk of incremental breakdown in the supply chain still exists.

Concern over the supply chain is a major reason why we add the word “cautious” to “optimism” when we talk about 2024.

The Geopolitical Wild Card

Never has a wild card been so wild before. Geopolitics continues to rear its head in the ugliest of ways, most recently with the Israel-Hamas War that many fear may escalate further. Ships have recently been slowed and sometimes been suspended from traveling the Suez Canal, clearly an example of how tumultuous geopolitics can impact the economy. Meanwhile, the Ukraine-Russia War sadly has no end in sight and the China-Taiwan situation remains politically fraught. Add to this what will undoubtedly be a headline grabbing 2024 presidential election in the United States, which could have enormous ramifications for energy transition.

While we believe fundamental drivers like interest rates and the supply chain are more meaningful to equity valuations, we’d be remiss to suggest geopolitics won’t have an impact. We certainly hope the only thing that breaks out is peace and prosperity in 2024, though at the moment it appears risk is skewed to the downside when it comes to geopolitics.

Positive outcomes on the above – declining interest rates, a healthy supply chain, and peace – would allow companies to exploit incentives provided in supportive public policy in the United States (e.g., the Inflation Reduction Act), Europe (e.g., Net Zero Industry Act), and across the world. This brings us back to déjà vu on the long-term outlook, especially now that eligibility rules are finally being published. This may ultimately eliminate another 2023 headwind, rule confusion. Finalizing the rules should drive visibility on returns for companies, increase the frequency of project announcements, and accelerate energy transition. The “green arms race” may have slowed in 2023, though make no mistake it’s just getting started.

Missed The Dip? No Worries, The Sector Is Still Cheap

The furious 4Q rally was nice to see. A vindication if you will of our view that interest rates were the major driver of weakness in renewables infrastructure. We hope you benefited from this reversal, though if you didn’t it is by no stretch too late. The sector is cheap. When everything comes together, like we hope it does in 2024, it should make for a highly favorable risk-reward proposition.

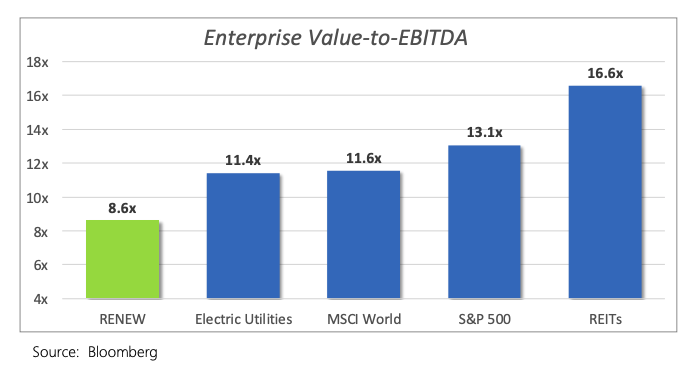

The EV/EBITDA of the Eagle Global Renewables Infrastructure Index (Bloomberg ticker: RENEW; Factset ticker: RENEWINDEX) trades at a 34% discount to the S&P 500, and a material discount to other income-oriented, value-focused investment opportunities, like Electric Utilities and REITs. We believe renewables infrastructure should trade in line at a minimum to these other sectors, given the sector’s unique setup to take advantage of what most believe is the pre-eminent megatrend over the next several decades.

2023 Recap: A Round Trip To The Starting Line

The Eagle Global Renewables Infrastructure Index (total return: +1%) underperformed the S&P 500 (total return: +26%). On an absolute basis the first half of the year was relatively boring, while the third quarter was full of despair, before a sharp reversal rally in the fourth quarter. After 12 months the index made essentially a round trip back to the starting line. Given all the headwinds faced by the industry, we believe this was a good outcome. We highlight three areas in particular: (1) the United States materially underperformed Europe, (2) the typically higher beta of pure-play renewable energy generation stocks was a determining performance factor, and (3) the RENEW Index outperformed virtually all other renewables-focused indices.

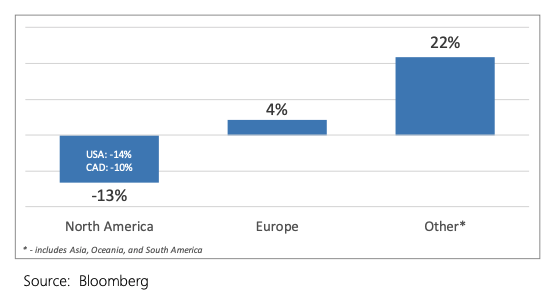

North America Materially Underperformed Europe

North America (-13%), particularly the United States (-14%), meaningfully underperformed Europe (+4%) and the globe (+22%). We believe regional exposure was the primary determinant of performance in 2023. It’s important to note the more mature nature of energy transition in Europe relative to the United States was likely significant, as well as varying degrees of government support in the fight against inflation.

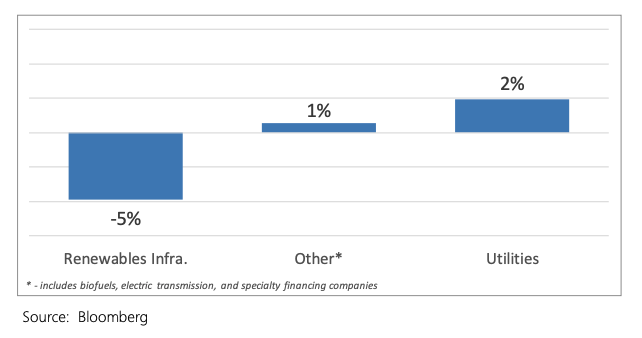

Defense Was A Winning Strategy In 2023

Playing defense earned investors outperformance in 2023. Pure-play renewables infrastructure stocks slipped 5% in 2023 versus a +2% rise for more defensive stocks like Utilities. As an example of this, ENEL (+34%) rallied hard while more pure-play stocks like Orsted (-41%) and AES (-33%) got slammed. To the extent 2024 is a “risk-on” year we would expect a reversal, that is pure-play stocks to outperform the more defensive Utilities. (Pure-play renewables tend to have a greater proportion of their assets and exposure in power generation like solar, wind, hydro, and thermal; Utilities tend to own assets like electric distribution that are highly regulated and less sensitive to energy transition.)

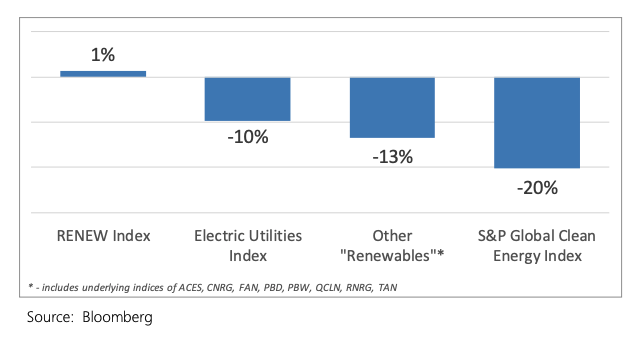

The RENEW Index Outperformed Virtually All Other Renewables Focused Indices

The RENEW Index generated positive absolute performance of +1% in 2023 on a total return basis.

This was substantially better than the performance of what we would consider its closest comparables. Whether you are a straight Utility investor (UTY: -10%) or more energy transition focused (S&P Global Clean: -20%; Other “renewables”: -13%) you’d have been better off investing in renewables infrastructure. One year does not make a trend or prove out a thesis, though it does support our opinion that renewables infrastructure ranks among the most compelling, risk-adjusted total return propositions for those interested in energy transition.

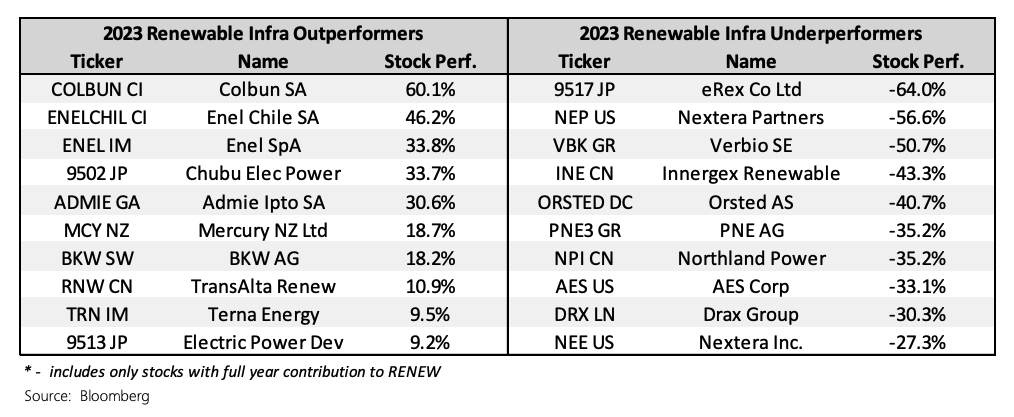

Finally, looking at 2023’s top outperformers and underperformers on a stock specific basis yields much of the same feedback. Europe was led by large-cap ENEL (~10.5% index weight) and offset by Orsted (~4% index weight) and Drax (~1% index weight), while Nextera (NEP/NEE: ~1.5%/~9.5% index weights) and AES Corp (~4% index weight) dragged down the United States.

We’re pleasantly surprised that despite the tremendous volatility and negative headlines experienced in 2023, the renewables infrastructure sector was able to generate positive absolute total return. We believe there is an enormous amount of support waiting in the wings for the tide to turn for renewables infrastructure and energy transition, and we’re cautiously optimistic this turn will happen in 2024.

Renewables Infrastructure Team Update

There were no significant team related news items to highlight this quarter. We continue to focus on the research and portfolio execution effort as well as our indexing initiative and are in constant dialogue with industry experts and management teams, both domestically and in Europe. We see the energy transition or de-carbonization megatrend continuing to gain traction among investors, supporting our view societal and political support are making renewable infrastructure increasingly inelastic to market forces.

– The Eagle Global Advisors Renewables Infrastructure Team

Disclosures

The indices shown are for informational purposes only and are not reflective of any investment. They are unmanaged and shown for illustrative purposes only. The volatility of the indices are likely materially different than the strategy depicted. Eagle Global’s Renewables Infrastructure Strategy includes buying and selling various renewables infrastructure companies. Holdings will vary from period to period and renewables infrastructure companies can have a material impact on the performance.

No Warranties. The accuracy and/or completeness of any Eagle Global Advisors index, any data included therein, or any data from which it is based is not guaranteed by Eagle Global Advisors, and it shall have no liability for any errors, omissions, or interruptions therein. Eagle Global Advisors makes no warranties, express or implied, as to results to be obtained from use of information provided by Eagle Global Advisors and used in this service, and Eagle Global Advisors expressly disclaim all warranties of suitability with respect thereto.

You Must Make Your Own Investment Decision. It is not possible to invest directly in an index. Index performance does not reflect the deduction of any fees or expenses. Past performance is not a guarantee of future returns. You should not make a decision to invest in any investment fund or other vehicle based on the statements set forth in this document, and are advised to make an investment in any investment fund or other vehicle only after carefully evaluating the risks associated with investment in the investment fund, as detailed in the offering memorandum or similar document prepared by or on behalf of the issuer. This document does not contain, and does not purport to contain, the level of detail necessary to give sufficient basis to an investment decision. The addition, removal, or inclusion of a security in any Eagle Global Advisors index is not a recommendation to buy, sell, or hold that security, nor is it investment advice.

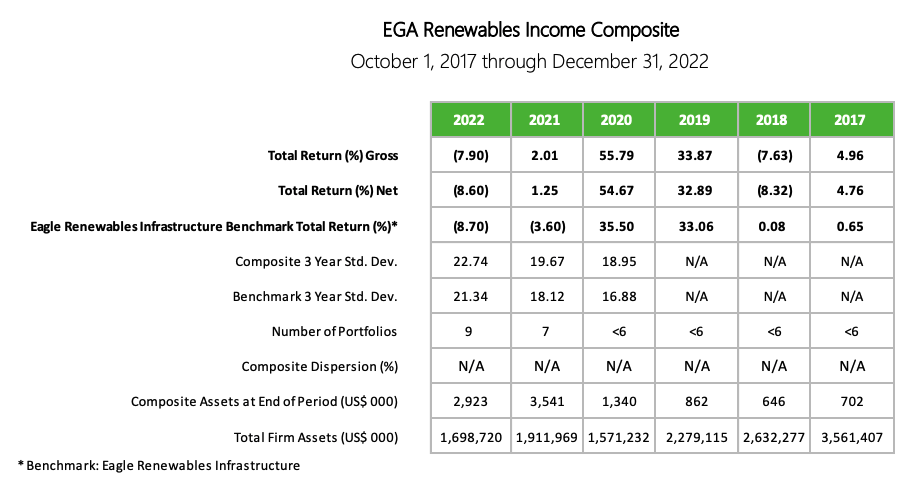

EGA Renewables Income Composite – The EGA Renewables Income composite consists of those equity-only portfolios invested in a concentrated portfolio of renewable infrastructure companies. • For GIPS purposes, Eagle Global Advisors, LLC is an independent investment advisor, registered with the SEC, actively managing individual investment portfolios containing domestic equity, international equity, master limited partnerships, and domestic fixed income securities, (either directly or through a sub-advisory relationship), for mutual funds, high net worth individuals, retirement plans for corporations and unions, financial institutions, trusts, endowments and foundations. SEC registration does not imply a certain level of skill or training. • Eagle Global Advisors, LLC claims compliance with Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with GIPS standards. Eagle Global Advisors, LLC has been independently verified for the periods 1/1/1997 to 12/31/2021. The verification reports are available upon request. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. Verification does not provide assurance on the accuracy of any specific performance report. GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. Only direct trading expenses are deducted when presenting gross of fee returns. In addition to management fees, actual client returns will be reduced by any other expenses related to the management of an account such as trustee fees or custodian fees. The reporting currency is the U.S. dollar. Returns are calculated net of non-reclaimable foreign withholding taxes on dividends, interest, and capital gains. Reclaimable withholding taxes are not accrued, but are cash basis as received. Eagle uses the asset-weighted standard deviation as the measure of composite dispersion of the individual component portfolio gross full period returns around the aggregate composite mean gross return. The 3 year annual standard deviation and internal dispersion are calculated using Gross of Fees returns. If the composite contains 5 portfolios or less (<=5) for the full period, a measure of dispersion is shown as not meaningful (N/A) and the number of portfolios is not reported. Past performance cannot guarantee comparable future results. All investments involve risk including the loss of principal. This presentation is only intended for investors qualifying as prospective clients as defined by GIPS. • The composite start date is October 1, 2017 and was created in 2020. The composite consists of separate accounts where the firm has full investment discretion, the portfolio contains over $100,000 in renewable infrastructure companies, and the portfolio properly represented the intended strategy at the end of the calendar quarter. All performance returns assume the reinvestment of dividends, interest, and capital gains. • The benchmark is the Renewables Infrastructure Index and is designed to track the performance of renewable infrastructure or renewable-related infrastructure assets, primarily wind, solar, hydro, biomass and electric transmission lines. Constituents are companies whose stocks trade globally in OECD countries. The index is a capped, float-adjusted, capitalization-weighted index developed by Eagle Global Advisors and disseminated real-time on a price-return basis (RENEW) and on a total-return basis (RENEWTR). • The indices shown are for informational purposes only and are not reflective of any investment. As it is not possible to invest in the indices, the data shown does not reflect or compare features of an actual investment, such as its objectives, costs and expenses, liquidity, safety, guarantees or insurance, fluctuation of principal or return, or tax features. Indices do not include fees or operating expenses and are not available for actual investment. Indices presented are representative of various broad based asset classes. They are unmanaged and shown for illustrative purposes only. The volatility of the indices is likely materially different than the strategy depicted. Eagle Global’s Renewables Infrastructure strategy include buying and selling various renewables infrastructure companies. Holdings will vary from period to period and non-renewables companies can have a material impact on the performance. • The Eagle list of composite descriptions is available upon request. Eagle policies for valuing portfolios, calculating performance and preparing compliant presentations are available upon request.