The market continues to confound investors, with the S&P 500 YTD total returns of approximately 19%[1], dramatically ahead of Wall Street’s full year estimates for 2023. Many are bracing for another meaningful selloff, while others are positioned as long as they have been in years. Allocating client portfolios in the face of this unpredictability is a serious challenge, especially for those who came into the year underweight equities.

One prominent solution is to change the structure of client exposures through the use of options. The proliferation of buffered products shows how much demand clients have for adding a little risk management to their market risk. If the market is going to sell off by another 20% this year, potentially cutting that loss in half helps clients feel more confident and reduces the risk of them making catastrophic decisions like selling at the lows.

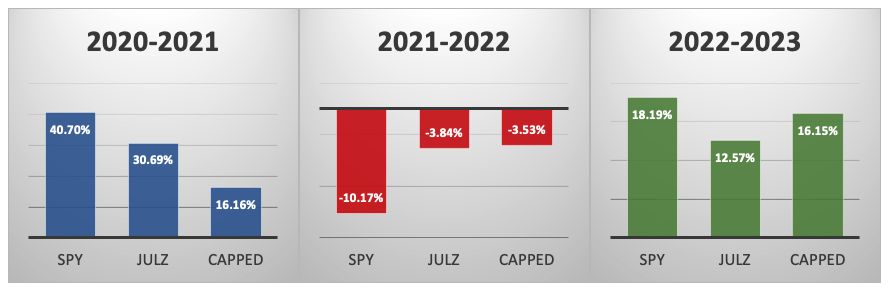

Asset flows into products with buffers have grown dramatically since the onset of the global pandemic, though largely in a format that limits upside potential. While buffers utilize put options to insure against certain levels of loss, call options are often used to generate the cash needed to buy that insurance. Too much of the industry has decided to cap the upside potential of what are ostensibly equity-linked products, and this has led to severe underperformance of equity benchmarks. For example, in the year ending June 30, 2021, the S&P 500 rallied by over 40%[2], while capped products underperformed by as much as 25 percentage points. Assuming an average annual S&P 500 total return of 9.6% implies a 2.4 year hole that has just been dug, with little chance of escape[3].

Instead of capping the upside of equity returns, another approach is a partial reduction in upside participation, without a hard limit. Altering the call positioning, specifically by removing the “cap”, will allow an investor to participate in the majority of the upside of stocks, with no limit, although only at a rate of 75-80% of the increase in prices. We feel these “uncapped buffer” products are a smarter way to allocate to equities as the potential for significant moves in either direction looms.

Source: Bloomberg

[1] Bloomberg SPXT INDEX as of 7/17/2023

[2] Bloomberg SPXT INDEX from 6/30/2020 – 6/30/2021

[3] Simple geometric return calculation solving for periods – implies needing an annualized 9.6% outperformance vs SPXT to break even (SPXT INDEX average yearly returns from 12/31/1992 – 12/30/2022)

An ETF wrapper may be the best solution, as capital gains can largely be deferred (allowing for further compounding of returns), and investors can avoid the burden of option paperwork at their custodians. Low investment minimums, daily liquidity, and the ability to buy into the market systematically over time are also benefits of this structure. The uncapped nature will benefit any investor looking to incorporate the “buffer” into their core equity allocation, as the ability to track the S&P more closely in all environments is proving to be a beneficial attribute.

With market prognosticators rushing to pump up their year-end estimates in light of the incredible first half of 2023, the potential for both continued upside or a market selloff exists. Adding a buffered and uncapped exposure to client assets could result in significant savings should a selloff occur while also providing the ability to participate in the market should we return to previous highs. Positioning clients in these products should serve investors well regardless of which direction Mr. Market chooses.

Call Options: Call options are financial contracts that give the option buyer the right but not the obligation to buy a stock, bond, commodity, or other asset or instrument at a specified price within a specific time period. The stock, bond, or commodity is called the underlying asset. A call buyer profits when the underlying asset increases in price.

Put Options: A put option (or “put”) is a contract giving the option buyer the right, but not the obligation, to sell—or sell short—a specified amount of an underlying security at a predetermined price within a specified time frame. This predetermined price at which the buyer of the put option can sell the underlying security is called the strike price.

Structured Outcome ETFs have characteristics unlike many other traditional investment products and may not be suitable for all investors. You should only consider an investment in the Fund if you fully understand the inherent risks, which can be found in the prospectus.

The Funds invest in options, which involves leverage, meaning that a small investment in options could have a substantial impact on the performance of the Fund. There can be no guarantee that a Fund will achieve its investment objective.